“They have the authority to arrest, but they’re not really trained to do so, since they’re licensed through the Department of Insurance!”

State Sen. Dan Claitor (R-Baton Rouge) is concerned the state lacks requirements for bounty hunters – also known as bail enforcement agents – to take the same firearms training as law enforcement. He’s authored SB 215 to require them to become POST certified (Police Officer Standards Training) and licensed via the Attorney General’s Office.

“Bounty hunters enter homes, put people in handcuffs, use tasers and use guns. When we grant arrest powers to anyone else in this state, we require them to be POST certified,” he told the Senate’s Judiciary C Committee.

“I haven’t heard any complaints of bounty hunters running amuck,” said Sen. Yvonne Colomb (D-Baton Rouge). “What’s the real reason you’re bringing this bill?”

“I admit, there have been no major incidents I’ve heard about here since 2011, but we need to get ahead of the situation before something bad happens again,” Claitor replied. And honestly, I don’t have faith in the state Insurance Department to do law enforcement.”

“I don’t have faith in this Attorney General,” Colomb came back.

“How long has the Department of Insurance been regulating bail bondsmen?” asked Sen. Troy Carter (D-New Orleans).

‘Since 1999,” Claitor answered.

“And how many incidents have there been since 1999 where that system ‘failed’?” Carter pressed.

“I don’t know of any, for certain,” Claitor replied. “Only that the regulations came to be because of something that originally took place in Caddo Parish.”

“So this isn’t an epidemic?” Carter concluded. “Why not do a study to see if a change is needed?”

Several dozen bail bond firms indicated opposition to shifting oversight for their industry away from the Department of Insurance, since they actually are insurance agents, representing insurance firms in a surety product. Sen. Fred Mills (R-Parks) asked those opposed if there was any parts of the bill they could work with.

“I would say no,” Guy Ruggiero, past president of Louisiana Bail Underwriters, said.

Bill Stiles, chief deputy Attorney General, also spoke in opposition, reminding the committee the Attorney General’s Office is not a regulatory agency, and therefore they don’t believe they are the appropriate agency to have this responsibility.

Ultimately, Sen. Claitor voluntarily deferred the bill “for another week, to rework it.”

Not long after, across the building in the House Commerce Committee, Rep. Blake Miguez (R-New Iberia) presented the topic that has him “up in arms.” Miguez’s HB 413 also involving firearms and the AGs Office.

“This aims to prohibit a financial institution from refusing services to those involved in firearms commerce,” Miguez said. “Recently, some big national banks told their clients to halt their sales of certain firearms, certain large-capacity magazines, certain types of ammo, or else they would be kicked out of services through the bank. Under this bill, if they discriminate, a complaint can be filed with the Attorney General, which would kick off an investigation, and could ultimately be taken to court.”

“To be clear, some institutions have mission statements, codes of ethics. Are you trying to prohibit that?” asked Rep. Cedric Glover (D-Shreveport).

“This is protecting small businesses from big financial institutions that make social policies that are discriminatory against Second Amendment Rights,” Miguez responded. “It’s a constitutional right, and they can’t get between you and those rights solely because you’re involved in the legal commerce of firearms.”

“What are some reasons that banks can refuse to do business with customers?” Rep. Edmond Jordan (R-Baton Rouge) asked.

“They can halt services as a legitimate business reason, due to financial or credit worthiness, or regulatory reasons. But they can’t tell a small business client no, just because the people that run the bank don’t like guns!” Miguez was adamant.

“This reminds of a bill brought here a few years ago because a gentleman didn’t want to bake cake for gay couple,” observed Rep. Patrick Connick (R-Marrero). “Isn’t this the same sort of thing?”

Connick was referring to then-Rep. (now Congressman) Mike Johnson’s HB 707 of the 2015 legislative session. Titled “The Marriage and Conscience Act”, it would have protected “the right of conscience, and the free exercise of religious beliefs and moral convictions.” It would have prohibited the state or any of its agencies from taking adverse action against those who asserted their moral convictions by denying services regarding marriages not between one man and one woman. That bill failed to get out of committee, and so, later in that same day, then-Gov. Bobby Jindal issued an executive order implementing the provisions anyway. Executive Order BJ 15-8 was rescinded with the April 2016 issuance of Gov. John Bel Edwards’ “Equal Opportunity and Non-Discrimination” order.

Miguez insisted the bills have more differences than similarities.

“That one was small business not wanting a particular client. This is about banks – highly regulated financial institutions – denying financial services to business for social issues. They are different issues,” Miguez asserted. “That was normal small businesses versus what we have here: the big banking industry deciding our entire social policy because they have leverage and power – because they have so much money.

“Don’t we, as people, have the right to chose not to do business with those whose policies we disapprove? asked Rep.Glover. “Consider the worldwide concern over blood diamonds, or our concerns here in Louisiana about catfish from Vietnam. With this bill, are we denying a conscientious business from establishing their own policies?”

“Where and by whom lettuce is harvested is not protected by constitutional right. Firearms are the purpose of the Second Amendment constitutional rights,” Miguez maintained.

“Free speech is a constitutional right, too,” Glover observed, gently. “Doesn’t this deny those rights?”

“This is different. It’s the Second Amendment, and it’s banks,” Miguez said. “This is tightly tailored to financial institutions which are already highly regulated.”

“So, under your bill, a gun dealer gets the right to decide who he or she will do business with – that is, sell weapons to – but the financial institution does not get the same right to decide?” Glover asked.

“They shouldn’t have higher power than the law. Louisiana made your Second Amendment rights absolute, and a financial institution cannot restrict that with their own policy,” Miguez said.

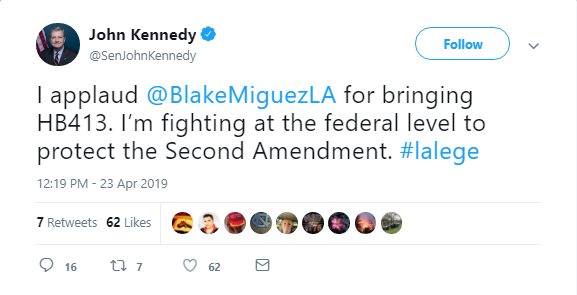

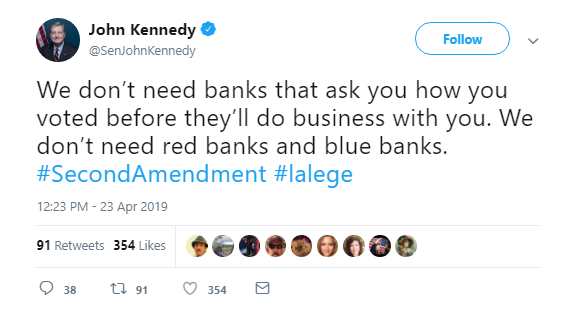

Throughout the discussion, Louisiana’s junior U.S. Senator John Kennedy, was tweeting commentary lambasting the banks. Kennedy has co-authored a similar federal bill, SB 821, the Freedom Financing Act, filed one month ago.

And without opposition Miguez’s HB 413 was advanced to the full House floor.